GST Update

Desk of CA Praveen Sharma – 920 Series (CAPS)

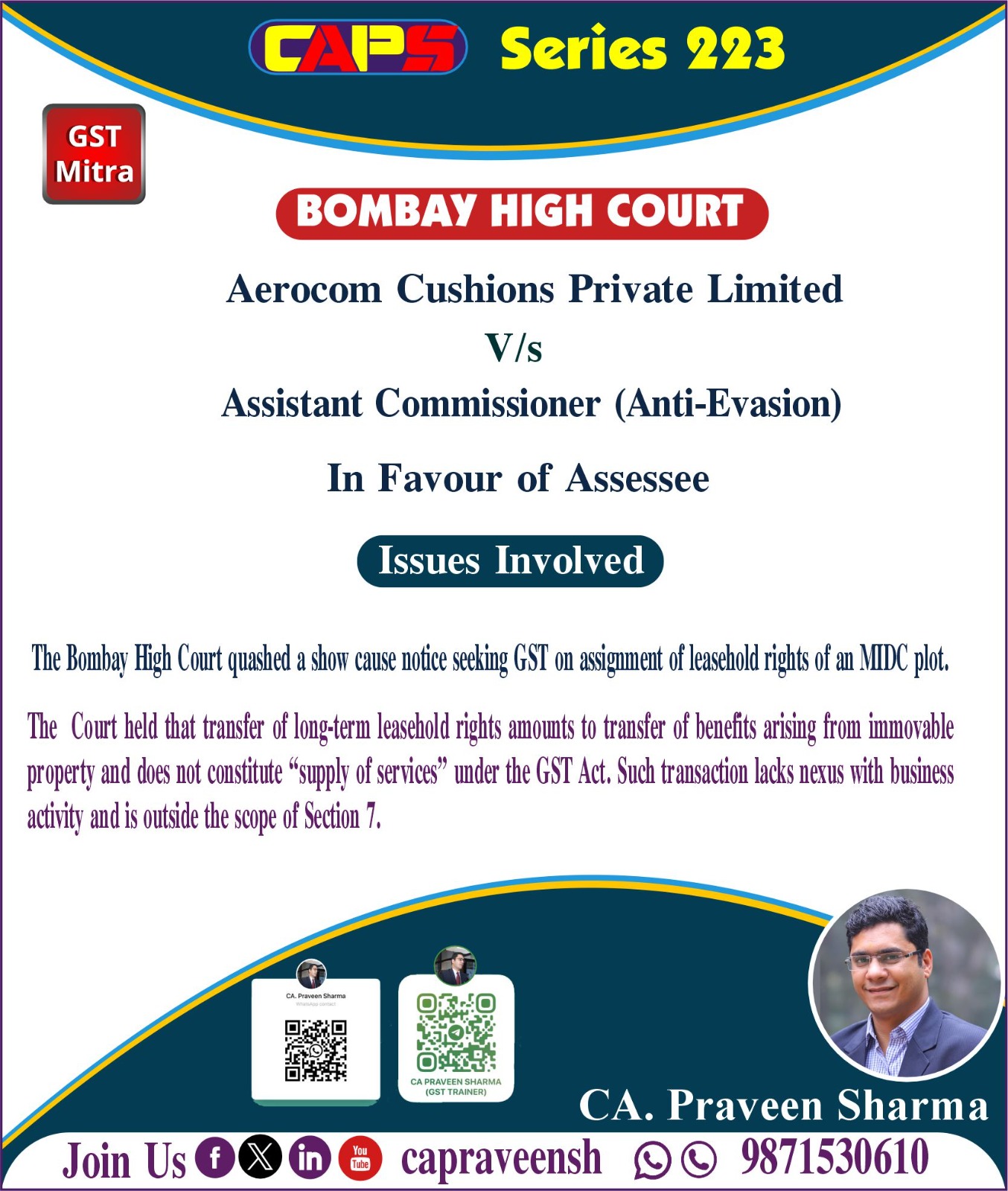

Bombay High Court in the case of Aerocom Cushions Private Limited

The Bombay High Court examined a GST show cause notice demanding ?27 lakh under Section 74 for alleged non-payment of GST on the transfer of MIDC leasehold rights.

The petitioner had assigned long-term leasehold rights of 95 years in an MIDC plot to a third party after obtaining prior approval from MIDC and paying the prescribed transfer premium.

The GST department treated this assignment as a taxable supply of services under Section 7 read with Schedule II of the CGST Act and classified it as “other miscellaneous services” taxable at 18%.

The Court observed that assignment of leasehold rights is neither a lease nor a sub-lease, as the original lessee’s rights are fully extinguished upon assignment.

It further held that entries relating to miscellaneous services cannot be stretched to cover transactions involving transfer of immovable property rights such as leasehold assignments.

The Court noted that the transaction amounted to a transfer of benefits arising from immovable property and had no direct nexus with business activity or furtherance of business.

Relying on an earlier Gujarat High Court ruling, the Court held that assignment of leasehold rights in land and buildings is not liable to GST.

Accordingly, the show cause notice was declared invalid and quashed, and the writ petition was allowed.

Link: CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: