GST Update

Desk of CA Praveen Sharma – 936 Series (CAPS)

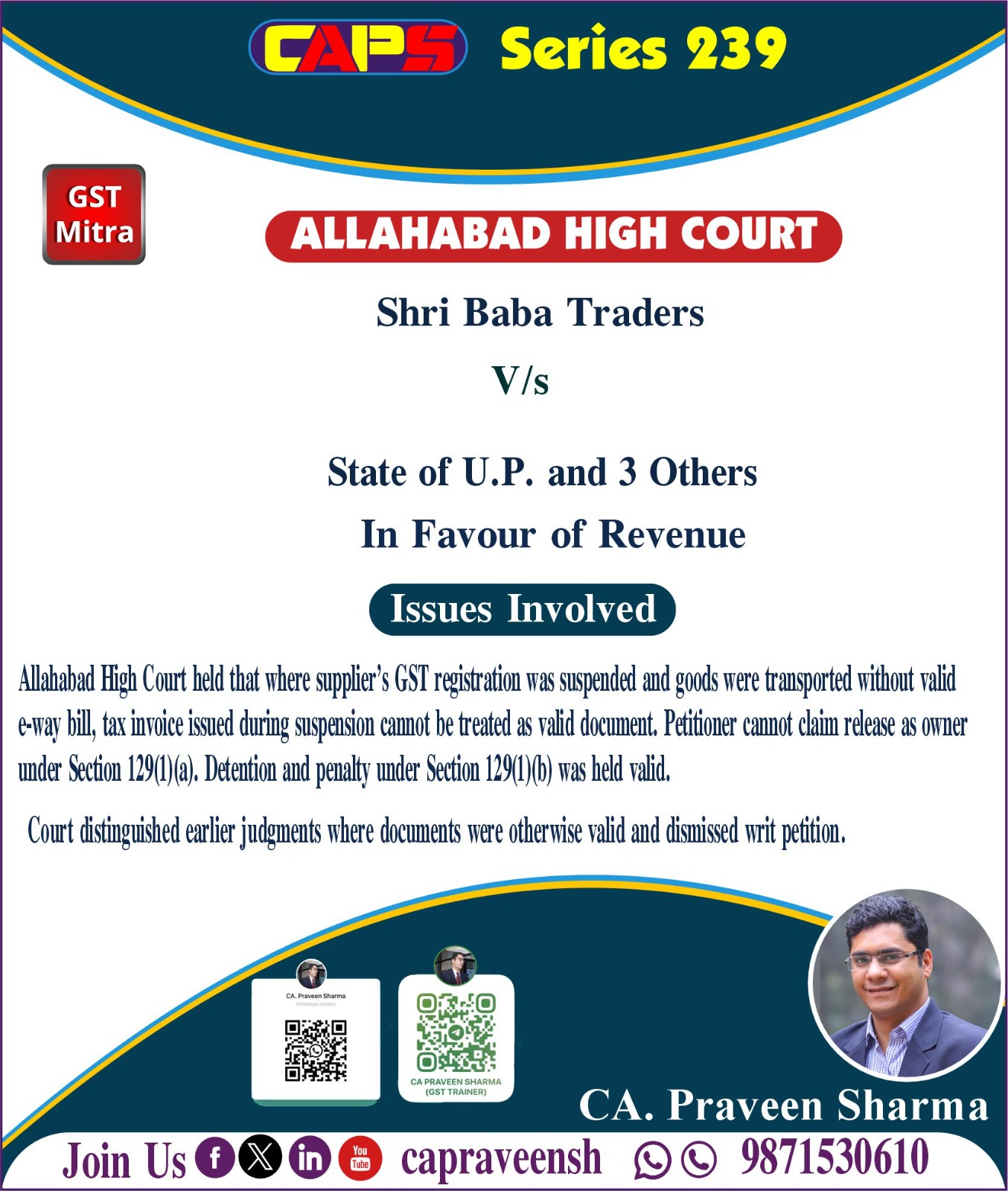

The Allahabad High Court decided two writ petitions together in the case of Shri Baba Traders as both matters involved similar issues related to detention of goods under GST.

The petitioner, a registered GST dealer engaged in trading of iron goods, had purchased material from a supplier based in Haryana. During transit, the goods were intercepted by the authorities because no valid e-way bill was found.

The petitioner argued that mere absence of an e-way bill should not result in seizure of goods. It claimed ownership and requested release of the consignment.

However, the State submitted that the supplier’s GST registration had already been suspended before issuing the invoice. As a result, the invoice itself was not valid, and legally no e-way bill could have been generated on the basis of such invoice.

In its reply, the petitioner admitted that the supplier’s registration was under suspension and that no e-way bill was generated for this reason.

The Court observed that when a supplier’s registration is suspended, it cannot issue a valid tax invoice. Therefore, the documents accompanying the goods were not legally acceptable.

Since there was no valid invoice or e-way bill at the time of transport, the authorities were justified in detaining the goods. The Court found no illegality in the action and dismissed both petitions.

LINK: CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: