GST Update

Desk of CA. Praveen Sharma – 943 Series (CAPS)

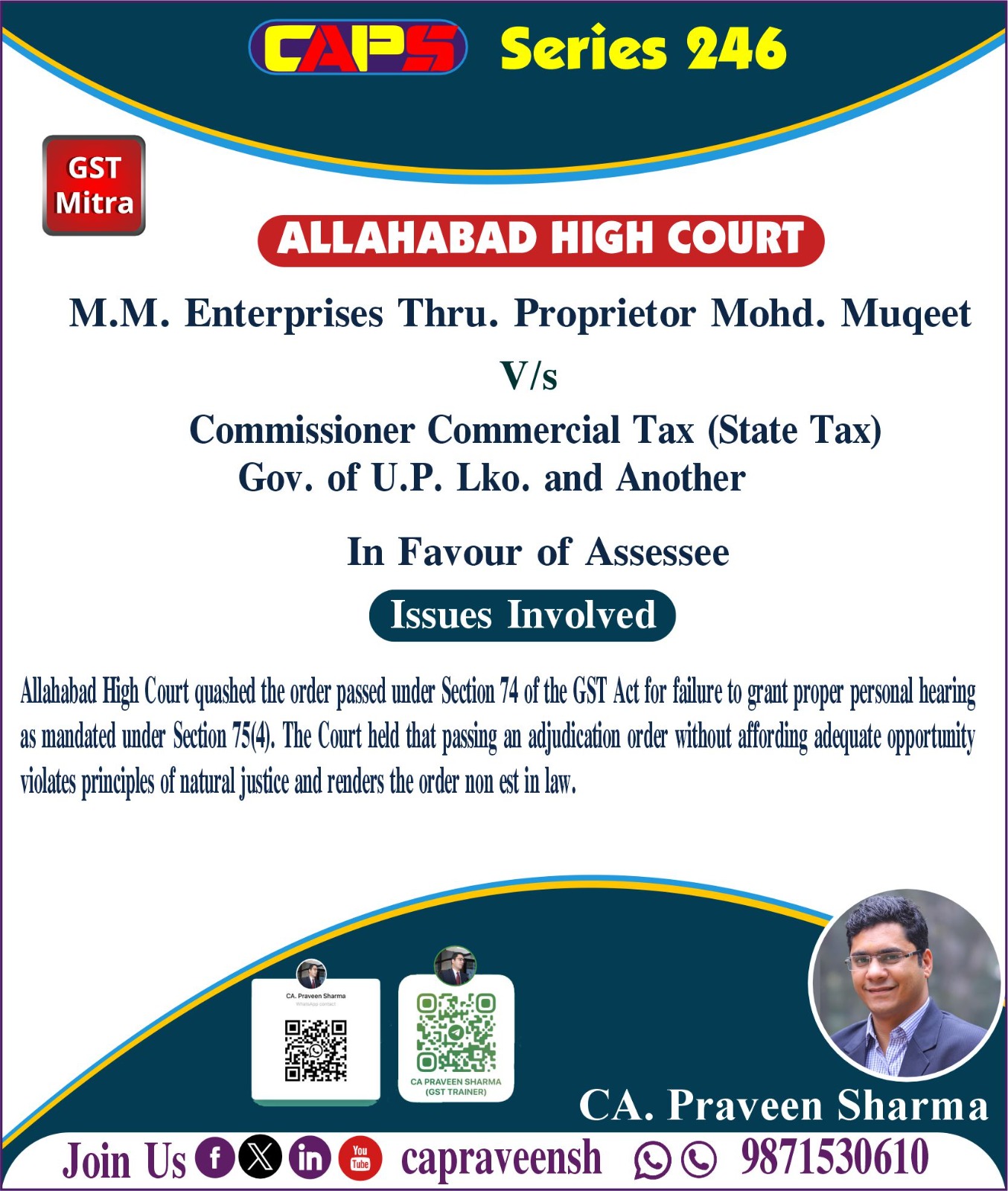

Allahabad High Court in the case of M.M. Enterprises Through Proprietor Mohd. Muqeet

In this case, the petitioner filed a writ petition before the Allahabad High Court under Article 226 of the Constitution challenging an order passed in Form DRC-07 by the Deputy Commissioner, State Tax, Lucknow. The order related to the tax period September 2021 to March 2022.

The main contention of the petitioner was that no effective personal hearing was granted as required under Section 75(4) of the CGST/UPGST Act. The petitioner argued that a proper opportunity to present the case was not provided before passing the final order under Section 74.

The Court examined the records and noted that a show cause notice had been issued on 27.08.2024 and a personal hearing was fixed for 23.12.2024. However, the petitioner did not appear on the scheduled date. Thereafter, the adjudicating authority passed the final order on 20.01.2025.

The Court observed that although a hearing date was earlier fixed, no fresh or specific intimation was given to the petitioner before passing the final order. Passing an order without granting a clear and effective opportunity of hearing was held to be a violation of the principles of natural justice.

Accordingly, the High Court set aside the impugned order dated 20.01.2025 and remanded the matter back to the concerned authority. The authority has been directed to provide a proper opportunity of hearing and then pass a fresh, reasoned order in accordance with law.

LINK:CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: