GST Update

Desk of CA. Praveen Sharma – 989 Series (CAPS)

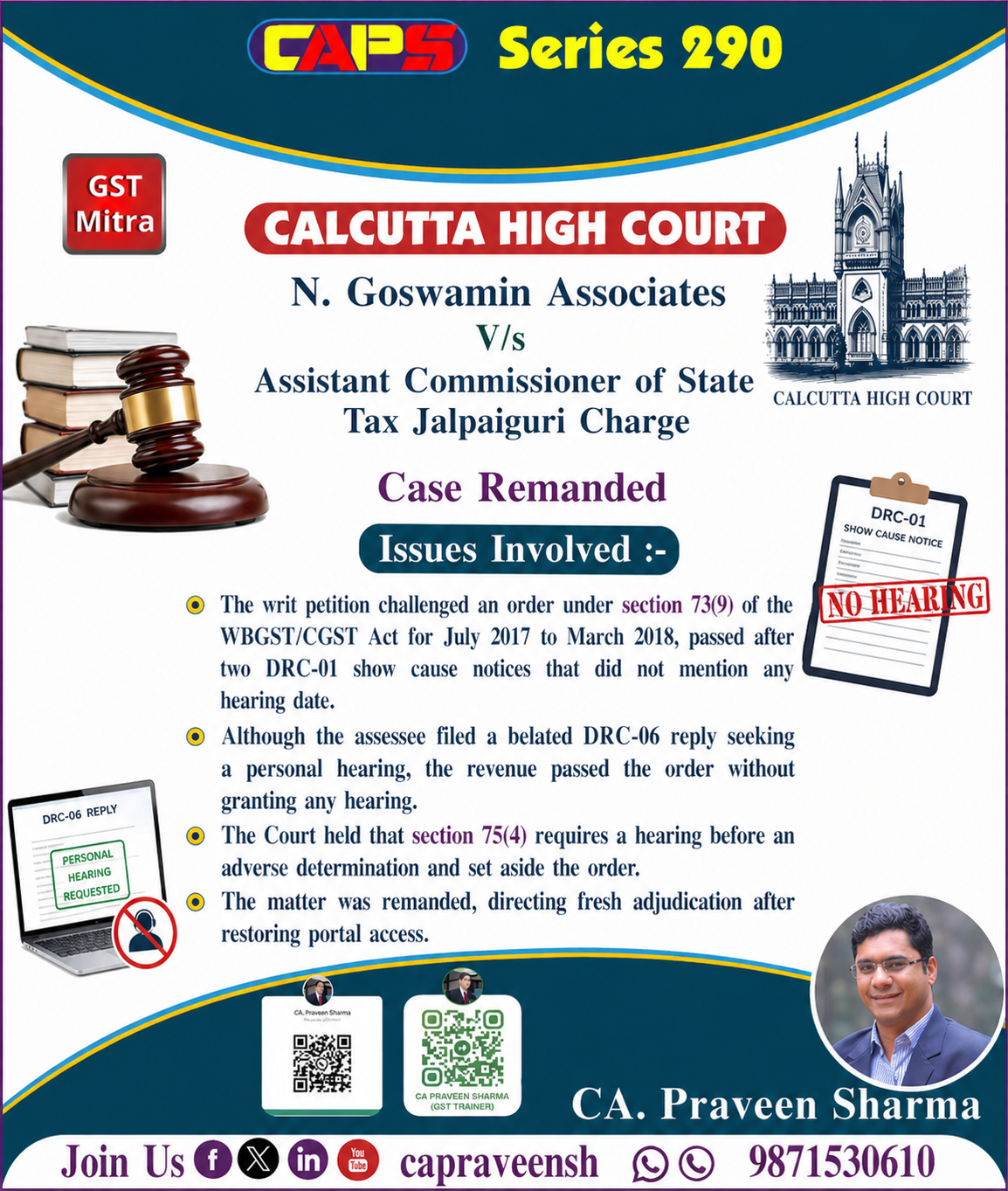

CALCUTTA HIGH COURT IN THE CASE OF N. Goswamin Associates

The writ petition challenges the order dated 29.12.2023 passed under Section 73(9) of the GST Act for FY 2017-18.

A show cause notice (DRC-01) was issued on 19.09.2023 for the period July 2017 to March 2018.

However, it did not mention the date of personal hearing. Later, another show cause notice for additional liability was issued on the same date, also without mentioning any hearing date.

The petitioner filed a delayed reply (DRC-06) on 31.10.2023 and requested a personal hearing, stating that he was unwell.

Despite this, the department passed the order on 29.12.2023 without granting any hearing.

The department argued that since the reply was delayed, no hearing was required.

The Court held that as per Section 75(4), granting an opportunity of hearing is mandatory before passing an adverse order, even if no reply is filed.

Since no hearing was given, the order was set aside on the ground of violation of natural justice.

The officer is directed to restore GST registration (if cancelled) only for completing proceedings and allow the petitioner to reply within 15 days.

Fresh hearing must be given and the matter decided again.

The writ petition is disposed of accordingly.

LINK:CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: