GST Update

Desk of CA. Praveen Sharma – 999 Series (CAPS)

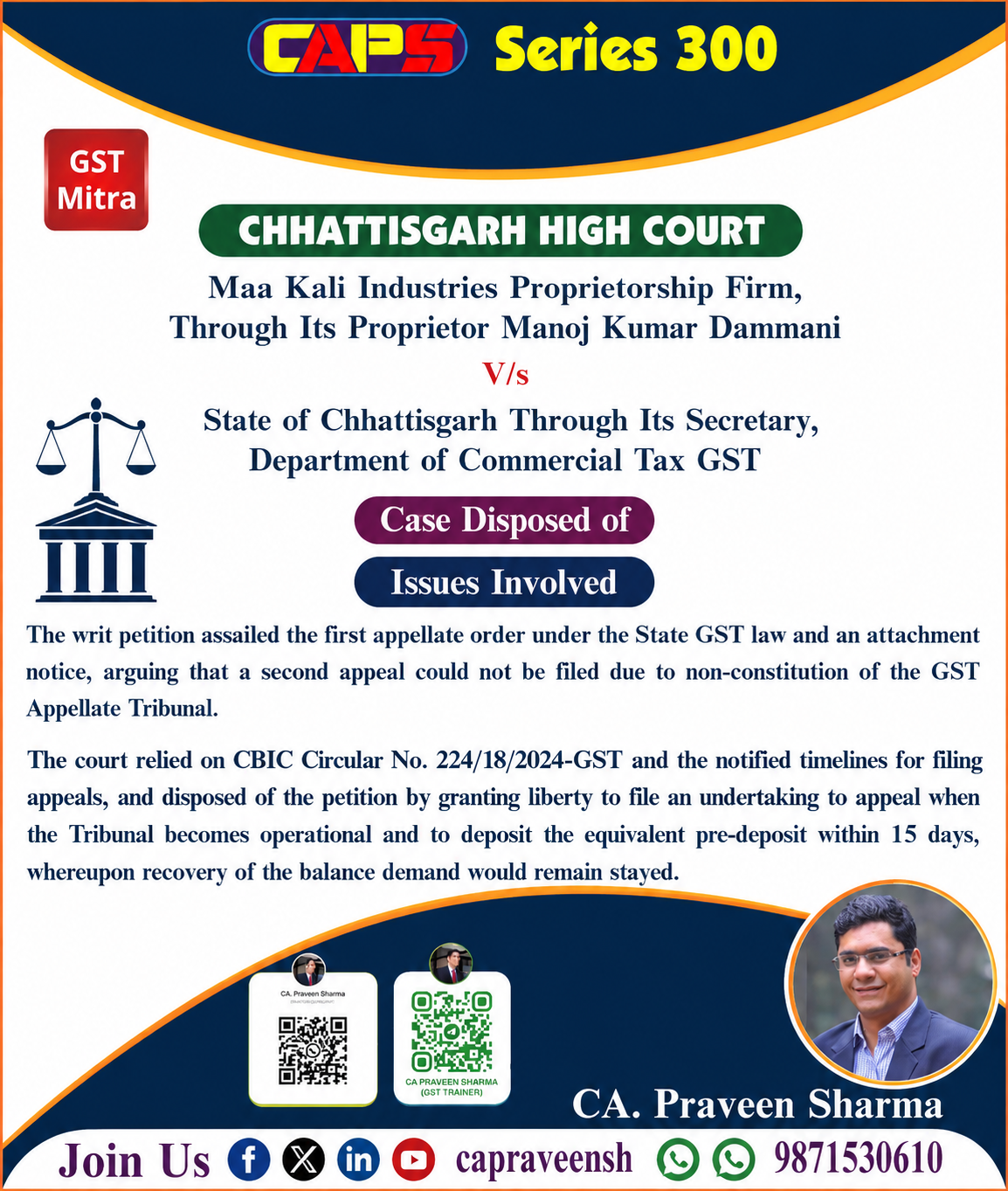

CHHATTISGARH HIGH COURT IN THE CASE OF Maa Kali Industries Proprietorship

The petitioner challenged recovery proceedings and earlier orders passed under the GST Act, along with an attachment notice.

The main issue was recovery of dues when the GST Appellate Tribunal was not functional.

The petitioner relied on CBIC Circular dated 11.07.2024, which provides guidelines in such cases.

As per the circular, a taxpayer can deposit the required pre-deposit amount even before filing appeal to GSTAT.

The circular also requires filing an undertaking that the appeal will be filed once GSTAT becomes operational.

It was clarified that upon payment of pre-deposit and submission of undertaking, recovery proceedings should remain stayed.

The government had also extended the time limit for filing appeals before GSTAT up to 30.06.2026.

The Court observed that clear guidelines already exist, so no detailed adjudication was required.

The petitioner was granted liberty to file undertaking and deposit pre-deposit within 15 days.

The Court directed that upon compliance, recovery of remaining demand shall remain stayed, failing which protection will lapse.

LINK: CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: