GST Update

Desk of CA. Praveen Sharma – 1001 Series (CAPS)

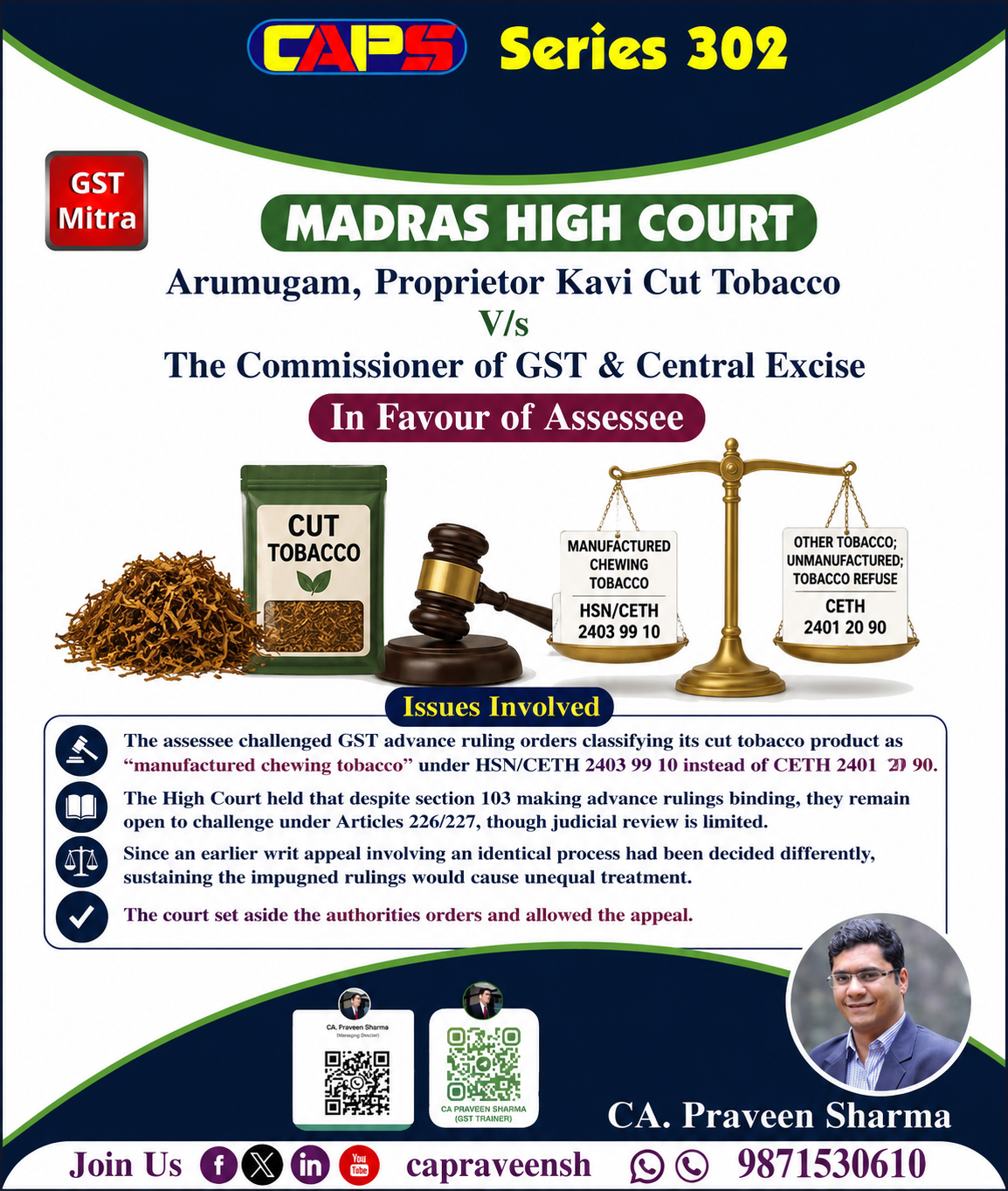

MADRAS HIGH COURT IN THE CASE OF Arumugam, Proprietor Kavi Cut Tobacco

The High Court dealt with a classification dispute involving a taxpayer engaged in the manufacture and sale of cut tobacco products.

The taxpayer claimed that the product should be classified under a lower tax category, while the department treated it as manufactured chewing tobacco attracting higher tax. The issue had already been examined by the Advance Ruling Authority and the Appellate Authority, both of which ruled in favour of the department.

The Court observed that although advance rulings are binding on the applicant and tax authorities, they can still be challenged before the High Court under writ jurisdiction.

However, the scope of such judicial review is limited and the Court does not act as an appellate authority but only examines whether there is any legal error, lack of jurisdiction or violation of natural justice.

In this case, the Court found that similar products manufactured through the same process had already been held to fall under a different classification in another case. Allowing conflicting classifications for identical products would lead to inequality and inconsistency in tax treatment.

Considering this, the Court set aside the orders of the Advance Ruling Authority, the Appellate Authority, and the earlier Single Judge order. The writ appeal was allowed to ensure uniform classification and to avoid discrimination among similarly placed taxpayers.

LINK:CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: