GST Update

Desk of CA. Praveen Sharma – 1009 Series (CAPS)

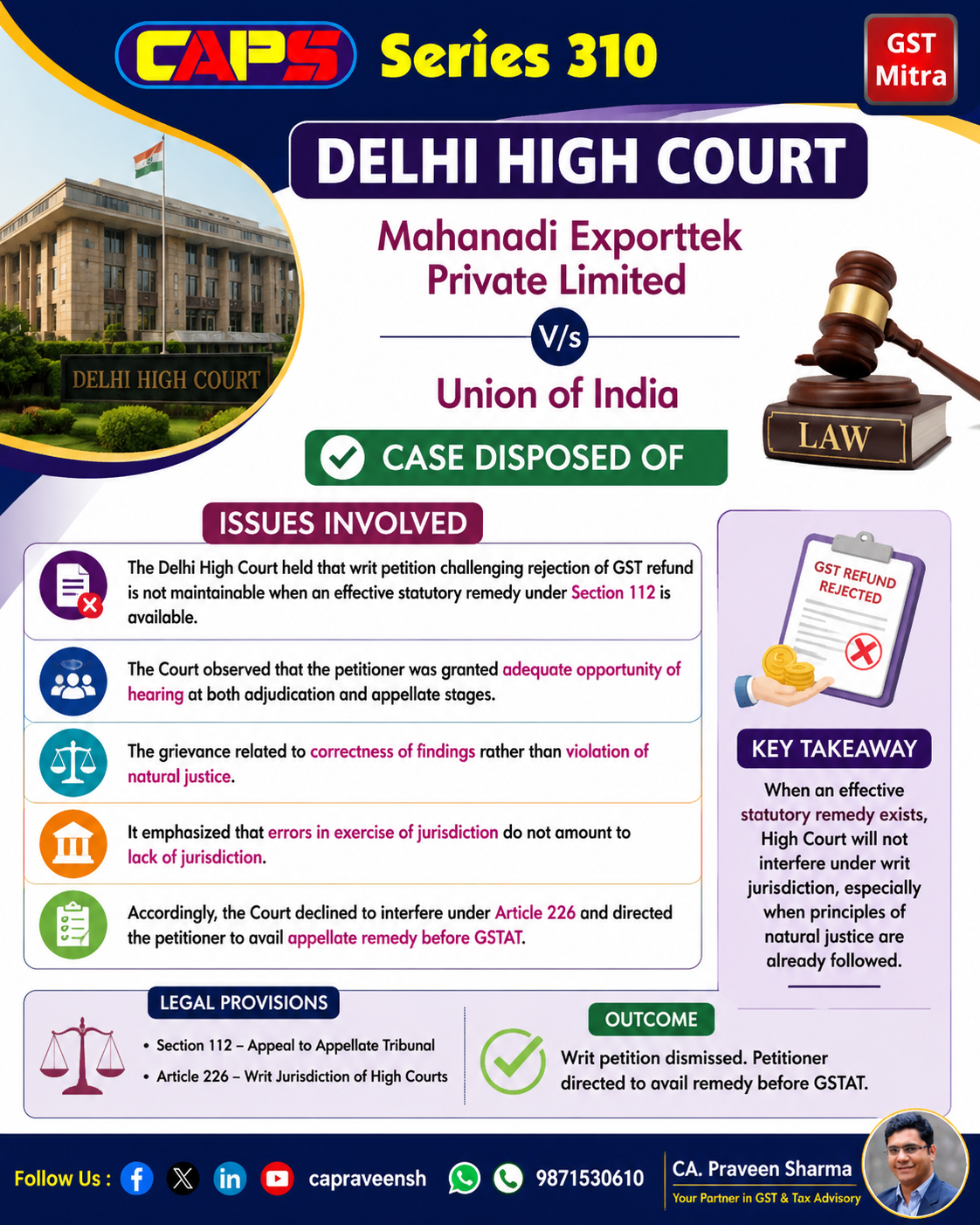

DELHI HIGH COURT IN THE CASE OF Mahanadi Export

The petitioner, a company engaged in export of electronic goods, challenged the rejection of GST refund claims amounting to over ?4 crore. The refund was denied by the department and later upheld in appeal on grounds such as non-submission of documents, DGARM alerts against suppliers, and doubts about transaction authenticity.

The petitioner argued that the rejection was based on issues not mentioned in the show cause notices, particularly DGARM alerts and alleged supplier irregularities, which violated principles of natural justice. It was also contended that no proper personal hearing was granted and that relevant documents like invoices, bank statements, e-way bills, and reconciliations were submitted but not considered.

The department opposed the petition stating that adequate opportunities were provided through notices, replies, and personal hearings. It was argued that the petitioner had failed to provide sufficient evidence to verify transactions and that the orders were reasoned and based on available material. The department also raised objection on maintainability, stating that an appeal before GSTAT was available.

The Court observed that there is a distinction between lack of jurisdiction and errors in exercising jurisdiction. It held that in this case, the authorities had jurisdiction and the dispute relates to correctness of findings rather than absence of authority.

The Court further noted that the petitioner was given opportunities to file replies and attend hearings at both original and appellate stages. Therefore, it was not a case of denial of natural justice but rather non-acceptance of the petitioner’s submissions.

On the issue of alternative remedy, the Court held that GSTAT is functional and an effective remedy is available under law. Hence, the writ petition should not be entertained when statutory appeal is available.

Final outcome: The Court declined to interfere and directed the petitioner to approach the GST Appellate Tribunal. The writ petition was disposed of without examining the merits of the case.

LINK:CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: