GST Update

Desk of CA. Praveen Sharma – 1014 Series (CAPS)

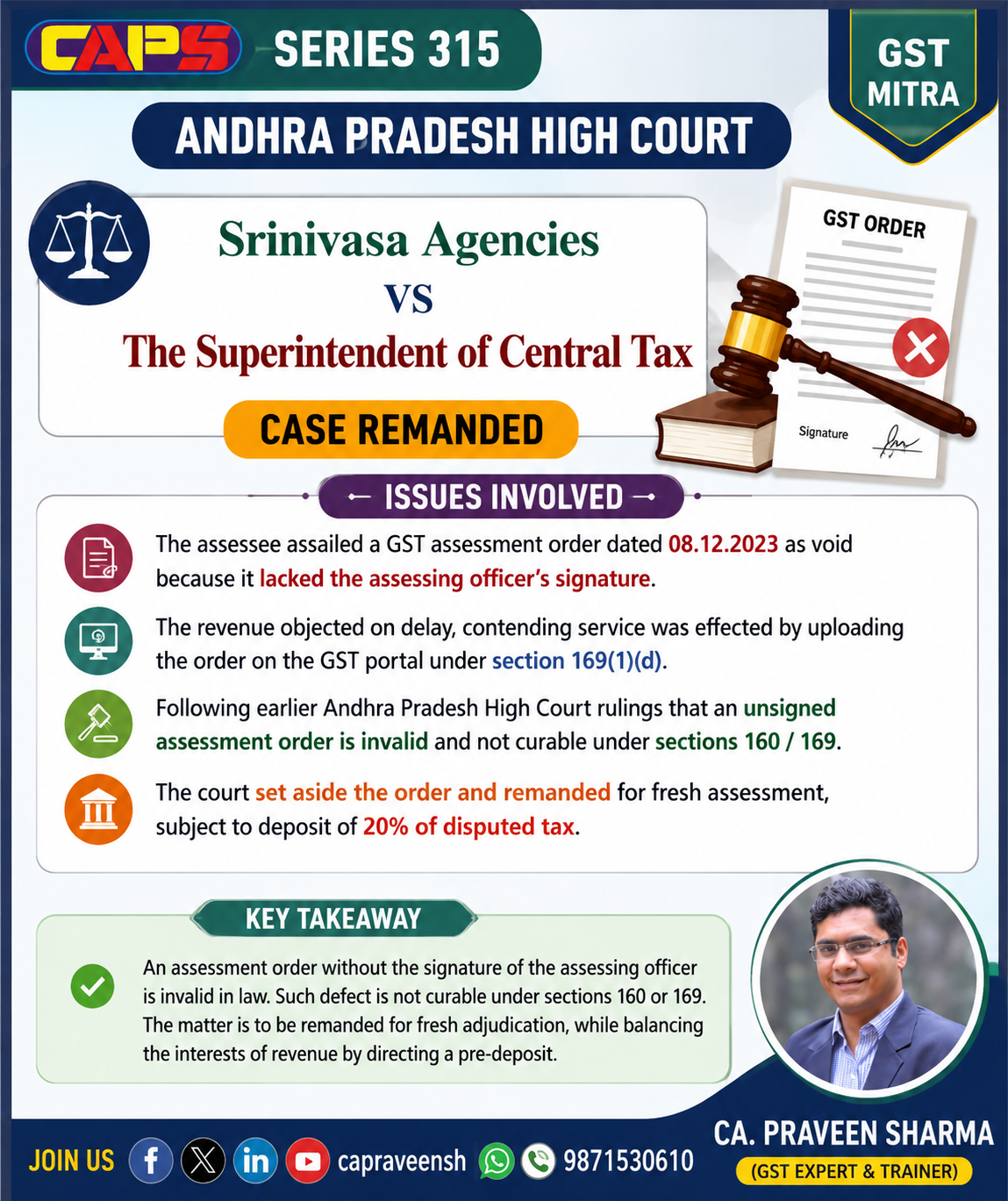

ANDHRA PRADESH HIGH COURT IN THE CASE OF Srinivasa Agencies

The petitioner approached the High Court challenging an assessment order on the ground that it did not contain the signature of the Assessing Officer. It was argued that an unsigned order is invalid and cannot be enforced.

The Court observed that earlier decisions have consistently held that the presence of a proper signature on an assessment order is mandatory. An order without signature cannot be treated as a valid legal document and is liable to be set aside.

On the issue of delay, the department argued that the order was served through the GST portal. However, the petitioner contended that the order was never received through conventional means. The Court noted that many taxpayers face practical difficulties in accessing portal communications and such factors cannot be ignored entirely.

Considering both the legal defect and the practical challenges faced by taxpayers, the Court set aside the impugned order and remanded the matter back to the Assessing Officer for fresh consideration after providing an opportunity of hearing.

However, to balance the interests of revenue, the Court directed the petitioner to deposit 20 percent of the disputed tax within a specified time.

Recovery proceedings initiated earlier were also set aside, and the matter was reopened for proper adjudication

LINK:CA. Praveen Sharma on Linkedin

Regards

CAPS

0 Comments: